Labor Market Softens Further as Unemployment Rises and Wage Growth Cools

As shutdown-delayed economic data continues to arrive, today’s BLS report delivered a hybrid look at October and November employment and detailed a labor market that is further softening. The November unemployment rate rose to 4.6%, up 0.2 percentage points from September and reaching its highest level since September 2021, when the labor market was still healing from the pandemic. Wage growth continued to cool as well, with average hourly earnings up just 0.1% month-over-month and 3.5% year-over-year.

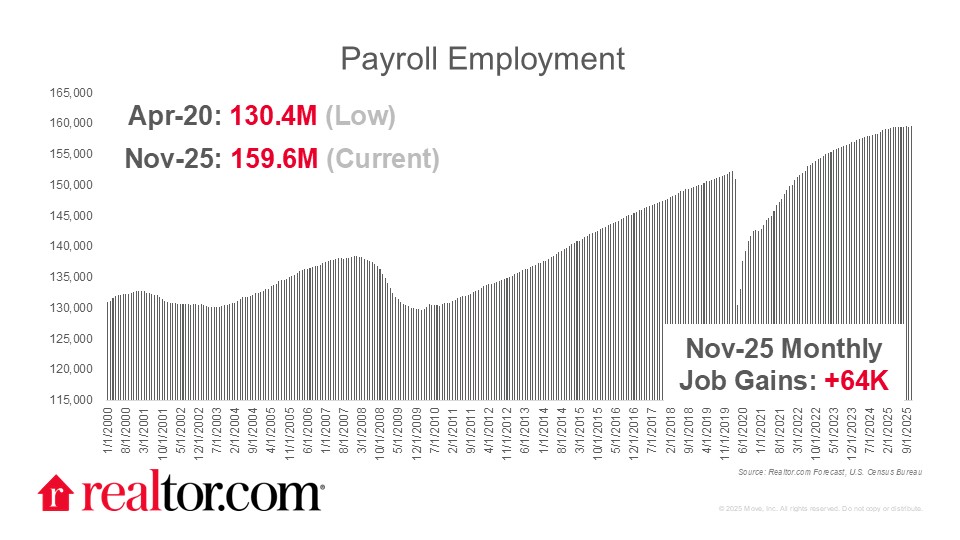

Modest Job Gains Mask Slowing Momentum and Fed Caution

November payrolls rose by just 64,000, while October showed a headline decline of 105,000, driven largely by an anticipated drop in federal government employment tied to deferred resignation buyouts. Stripping out government effects, private-sector job growth was modest but positive, with +52,000 jobs in October and +69,000 in November. By the Fed’s own framing, growth at that pace might actually signal a slowdown rather than resilience. Chair Powell has said the Fed is effectively adjusting payroll gains downward by roughly 60,000 jobs in anticipation of future revisions, meaning today’s private sector gains are not likely to mean much to policymakers. Although there was no unemployment rate reading for October due to the shutdown, most signs point to a low-momentum labor market that has slowed materially from earlier in the year.

For Housing, Demand Fundamentals Matter More Than Near-Term Rate Moves

For housing, today’s numbers underscore that the story is less about imminent rate cuts and more about demand fundamentals. Mortgage rates have moved largely sideways despite recent Fed easing, underscoring Powell’s point that monetary policy operates on short-term rates, not mortgages. A softer labor market could blunt near-term housing demand by weighing on household confidence and income growth, as the Fed gathers more data before deciding their next move. At this slow point in the housing calendar, affordability, rate lock-in, and undersupply remain the dominant constraints. Looking ahead, lower rate forecasts for 2026 support a modest rebound relative to 2025, but with mortgage rates still expected to hover near current levels, affordability will stay front and center. That continues to favor lower-cost “refuge markets,” and it reinforces a core reality: a stable labor market will do more to support housing demand than mortgage rates moving a few basis points.

Subscribe to our mailing list to receive updates on the latest data and research.

{kind=link}